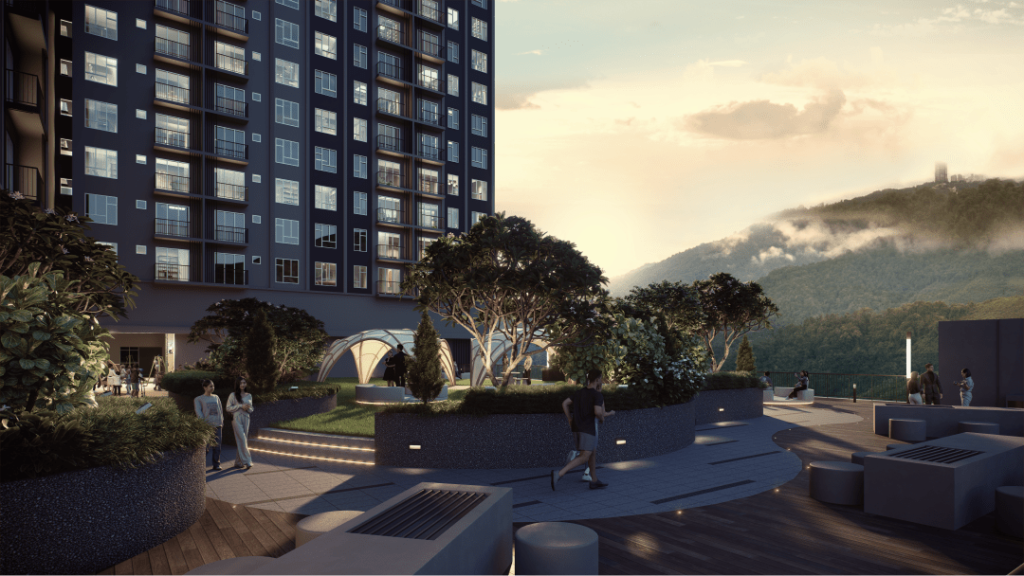

Centrum Iris A Premier Destination That Redefines Highland Living In Cameron Highlands

Thinking of a cool, refreshing escape to the highlands? Or perhaps you’re planning to grow your business in a vibrant, high-traffic area? Either way, Centrum Iris could be just what you’re looking for. Located right in the heart of Brinchang’s bustling commercial district, Centrum Iris offers more than just a prime address. It brings together […]

Buying a House – A Need or a Must in Malaysia Today?

For many Malaysians, the dream of owning a home has long been a symbol of stability, success, and financial security. But in today’s rapidly changing economic landscape, is buying a house still just a need, or has it become a must? With rising property prices, evolving lifestyles, and government incentives, let’s explore why homeownership is […]

The Strategic Value of Interpersonal Communication in the Property Sector

In the dynamic property sector, effective interpersonal communication is a critical enabler of business success. It serves as the foundation for building client relationships, fostering internal collaboration, and navigating complex negotiations. Professionals who master this skill gain a competitive edge by enhancing stakeholder engagement, ensuring seamless operations, and driving long-term business growth. Trust is a […]

LBS Unveils Ambitious 8 x 8 Strategy for 2025 – 2027 in Property Development

LBS Group has revealed its bold 8 x 8 Strategy during its Town Hall Meeting 2025. The strategy aims to elevate LBS’s position as a market leader, moving the company towards new heights of achievement and industry innovation. With a total gross development value (GDV) of approximately RM8 billion set to be rolled out across […]

Welcoming 2025: A Bright New Chapter with LBS

Hello, 2025! As we step into a fresh new year, we at LBS Bina Group can’t help but reflect on how incredible 2024 was. Winning the title of Malaysia’s Best Managed Companies for the third consecutive year was a proud moment, and it inspires us to aim even higher. Among our greatest achievements, we are […]

Investing In Bayu Hills For Long-Term Gains

Located in the serene, eco-conscious town of Rimbawan at Genting Highlands, Bayu Hills is a high-rise residential development by LBS that presents an investment opportunity. Here are several reasons why purchasing a property in Bayu Hills is a smart investment for both rental opportunities and future capital appreciation. 1. Cool, Fresh Weather Year-Round Rimbawan is […]

Embrace Sustainable Living: Join the Green Revolution at SkyRia @ D’Island Residence

In an exciting move towards a greener future, LBS Bina Group has teamed up with RHB Banking Group to launch innovative green financing solutions for the remarkable SkyRia @ D’Island Residence in Puchong. This strategic collaboration isn’t just about homes; it’s about creating a vibrant, eco-friendly community where sustainable living becomes a reality. SkyRia has […]

Perks And Plusses Turns One Celebrating a Year Of Exclusive Rewards and Epic Giveaways!

On 27th August 2024, we proudly celebrate the exciting first anniversary of Perks & Plusses, LBS Bina Group Berhad’s groundbreaking loyalty program! In just one year, Perks & Plusses has revolutionized the way our homeowners experience exclusive rewards and benefits, quickly becoming a favorite among LBS homebuyers. To celebrate this exciting milestone, we’ve lined up […]

Essential Considerations for Buying Your Dream Home in 2025

Are you a Gen Z born between 1997 and 2012, constantly on the lookout for your dream home in the upcoming year? As we all know, buying a house is a significant financial and personal decision. Here are several key factors to consider if you are planning to buy a house in 2025. Financial Readiness […]

Key Factors to Consider When Deciding on a House Renovation

A typical scene in one of P. Ramlee’s famous movies shows how a family always tries to compete with their neighbors when they see them getting a new sofa or starting to renovate their house. In reality, the urge to purchase new furniture or decide to renovate the house is heavily influenced by lifestyle and […]